A cheaper workers’ compensation premium can sometimes hide a much bigger liability problem.

You may have been encouraged by an accountant, business adviser, lawyer or other consultant to separate parts of your business into different entities as a way to manage risk, protect assets and simplify your operating structure.

On paper, this can look neat: one entity owns the assets, another runs the operations and another employs the staff. In higher-risk industries such as construction, roofing, manufacturing, transport and labour-intensive trades, this kind of structure may even be suggested as a way to better manage payroll classifications and insurance costs.

But there is a major insurance risk that is often missed.

A structure that appears to reduce workers’ compensation costs can create a much larger exposure under Public Liability Insurance or General Liability Insurance.

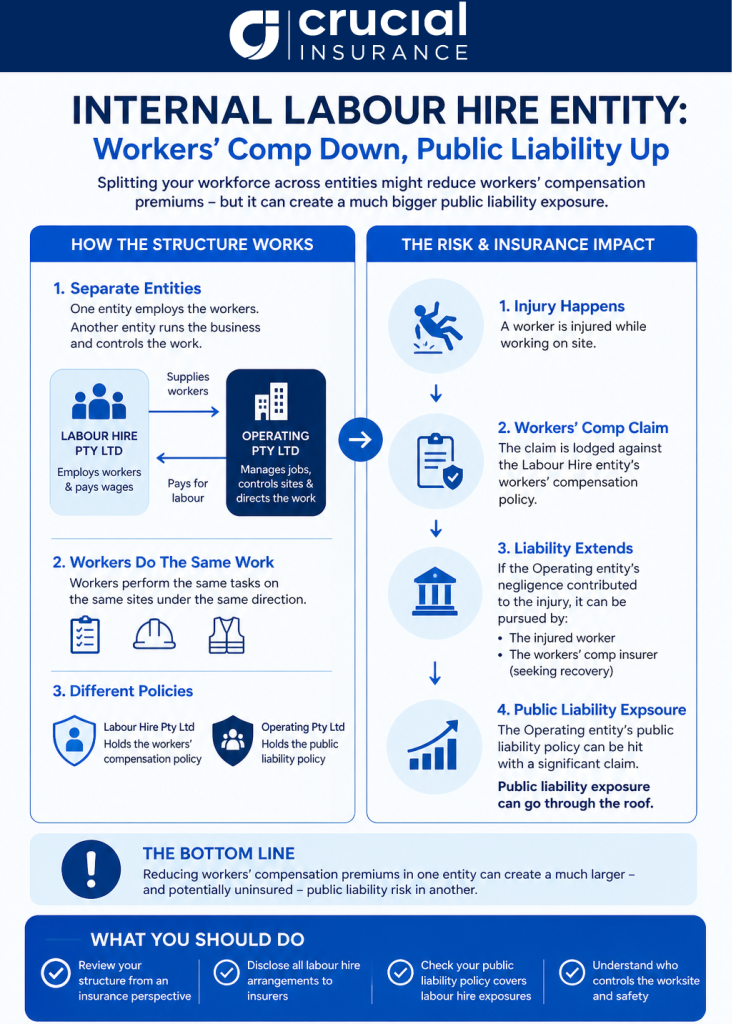

How the internal labour hire structure works

A common version of this arrangement involves creating a separate entity, for example, “Labour Hire Pty Ltd,” which employs the workers and supplies them to another related entity in the same business group.

The operating entity may still run the jobs, control the worksites, direct the labour and deal with clients. But the workers are technically employed by the separate labour hire entity.

In Queensland, WorkCover uses WorkCover Industry Classification codes to group businesses and calculate premiums. WorkCover also has specialised classifications for labour hire businesses, including classifications for administrative staff and classifications based on the industries where workers are placed.

For some businesses, this may create a perceived opportunity to break payroll into different categories. For example, a construction business may want to separate roofing workers, clerical staff, supervisors or other labour types more clearly.

But the insurance outcome is not always as simple as moving wages into a different box.

And here’s your dilemma: workers’ compensation may go down, but in return, Public Liability may go up.

When workers are employed by one entity and supplied to another related entity, the operating entity may become the “host employer” in practical terms.

That matters because the host entity may be responsible for the worksite, supervision, safety systems, equipment, inductions and day-to-day direction of the worker. WorkSafe Queensland notes that, in labour hire arrangements, the labour hire provider is the legal employer, but host employers still have obligations to cooperate with rehabilitation and return-to-work processes for injured labour hire workers.

The bigger issue is liability.

If a worker is injured, they may claim through the labour hire entity’s workers’ compensation policy. But depending on the circumstances, the claim may not stop there. The injured worker, or the workers’ compensation insurer, may pursue the host entity if the host’s negligence contributed to the injury.

That is where Public Liability or general liability insurance comes into play.

Berkley Insurance Australia has warned that internal labour hire structures can lead to claims against the parent group’s general liability policy from both the workers’ compensation insurer seeking recovery and the injured worker pursuing a civil claim.

In other words, the business may have shifted the workers’ compensation exposure away from the operating entity, only to create a larger liability exposure for that same operating entity.

Why insurers care about this

From an insurer’s perspective, labour hire arrangements can materially change the risk.

The host employer may be the party with the greatest practical control over the work being done. It may control the site, the system of work, the supervision and the equipment. Berkley notes that the greater the utility a host employer gets from labour hire arrangements, the greater the general liability exposure it may accept. It also notes that host employers often bear a significant proportion of damages because they control the environment, direction and safety systems.

That means Public Liability insurers may treat labour hire or internal labour hire arrangements as a significant underwriting issue.

If the business has not properly disclosed the arrangement, there may be serious problems when a claim occurs.

Coleman Greig Lawyers also warns that host employers can fall into the trap of being uncovered by Public Liability Insurance when labour hire employees make claims, and says host employers should disclose the use of labour hire employees on their Public Liability policy.

The “same worker, two policies” problem

One of the uncomfortable features of internal labour hire structures is that the same group of workers can end up touching multiple insurance policies.

The labour hire entity may hold the workers’ compensation policy because it is the legal employer.

The operating entity may hold the Public Liability policy because it controls the worksite and is exposed to third-party injury claims, including claims involving labour hire workers.

That can create disputes between entities, insurers and policies over who is responsible, who should respond and how liability should be shared.

This is not always predictable. HWL Ebsworth has noted that courts may apportion liability between labour hire employers and host employers by looking at how each party departed from the reasonable standard of care and the significance of each party’s negligence. That assessment involves broad discretion, which can make outcomes difficult to predict.

For business owners, that means a structure designed to simplify costs can create more complicated claims.

A simple example

Imagine a roofing business creates a separate company to employ its workers.

The employment entity pays the roofers and holds workers’ compensation cover. The operating entity wins the contracts, manages the jobs, controls the sites and directs the roofers day to day.

A roofer falls from height and suffers a serious injury.

At first, the claim may sit under the employment entity’s workers’ compensation policy. But if the operating entity controlled the unsafe worksite, failed to provide proper fall protection, or directed the work in a way that contributed to the injury, the operating entity may also be drawn into the claim.

The result?

The business may have reduced one workers’ compensation premium, but created a major Public Liability claim against another entity in the group.

In the end, what was envisioned as a way to reduce costs doesn’t reduce costs at all.

This isn’t just a paperwork issue

Labour hire is not simply a label. Fair Work explains that labour hire involves one business providing workers to another business, with the labour hire employer paying the employees while they work for the host. Fair Work also distinguishes this from a services contract, where a business takes on part of the work itself rather than merely supplying labour.

This distinction matters, because if a business creates an internal labour hire structure in name only, while the same people still work in the same way, under the same control, on the same sites, the insurance and legal consequences still need to be considered carefully.

Insurers will want to understand the real arrangement, not just the corporate diagram.

What you should consider before restructuring

Before creating a separate labour hire, payroll or employment entity, you should ask:

- Has the structure been reviewed from an insurance perspective, not just an accounting or legal perspective?

A structure that looks efficient on paper may create unexpected liability exposures. A quick conversation with a qualified and experienced Business Insurance Broker (such as Crucial Insurance!) can help answer this question.

- Have all insurers been told?

Workers’ compensation, Public Liability, Management Liability Insurance and contract works insurers may all need to understand the arrangement.

- Does the Public Liability policy respond to labour hire worker injury claims?

Some policies may exclude or restrict cover for worker-to-worker, labour hire or contractor injury claims.

- Are indemnity clauses enforceable?

Labour hire companies and host employers can share liability, and that indemnity clauses may not always hold up, particularly in Queensland and Victoria workers’ compensation contexts.

- Who controls the worksite and safety systems?

The entity with practical control may carry a large share of liability, regardless of which entity technically pays the worker.

- Has the premium saving been compared against the increased liability exposure?

A lower workers’ compensation premium may not be beneficial if it causes a larger Public Liability premium, higher excess, reduced insurer appetite or uncovered claims. A business will also need to factor in the additional insurance premium for the Labour Hire entity. This will include specialist Labour Hire Public Liability and Professional Indemnity insurance..

Here’s what’s important

Creating an internal labour hire entity can seem like a clever way to manage payroll, workers’ compensation classifications and business structure.

But it can also create a serious Public Liability exposure.

The danger is that business owners may focus on the visible saving while missing the hidden risk. Workers’ compensation may reduce, but the Public Liability exposure may increase dramatically, especially if the operating entity controls the worksite and safety systems. This can result in many insurers declining to provide terms for Public Liability insurance which leads to significant premium increases where coverage can be obtained.

For industries where injuries can be severe, such as roofing, construction, manufacturing, logistics and labour hire, this is not a minor technical issue. It can affect claim outcomes, premiums, excesses, insurer appetite and whether the right policy responds when something goes wrong.

Before making structural changes, businesses should speak with an insurance adviser who understands workers’ compensation, Public Liability and complex business structures.

At Crucial Insurance, we help businesses look beyond the surface of their insurance program so they can understand where risk is actually sitting, not just where it appears to sit on paper.

This article was written by Tony Venning,

This article was written by Tony Venning,

Managing Director at Crucial Insurance and Risk Advisors.

For further information or comment please email info@crucialinsurance.com.au.

Important Disclaimer – Crucial Insurance and Risk Advisors Pty Ltd ABN 93 166 630 511 AFSL 45150. This document provides information rather than financial product or other advice. The content of this document, including any information contained on it, has been prepared without taking into account your objectives, financial situation or needs. You should consider the appropriateness of the information, taking these matters into account, before you act on any information. In particular, you should review the product disclosure statement for any product that the information relates to it before acquiring the product.

Information is current as at the date documents are written as specified within them but is subject to change. Crucial Insurance, its subsidiaries and its associates make no representation as to the accuracy or completeness of the information. All information is subject to copyright and may not be reproduced without the prior written consent of Crucial Insurance.